Learning How to Budget your personal finance budget is by far the greatest financial asset you can develop. Irrespective of your salary level or current position, it won’t help you in any way to try sticking to the principle of ‘it doesn’t matter’ here. A budget shouldn’t limit your choices and opportunities far from that it will provide your finances with direction.

Frankly speaking, it doesn’t take much for the majority of us to end up struggling financially in the next month something we might not be fully aware of.

No emergency fund, no savings plans. Unclear expenditure pattern. Only salary inflow… and somehow, at the end of each month, nothing left.

And there are plenty of us who could relate to this. Which, fortunately enough, means that this problem isn’t beyond solution.

In the course of this post, we will look into all details of developing a proper personal finance budget, including such aspects as the popular 50-30-20 rule, actual budgeting tools, finance management strategies and techniques, etc.

What Is a Budget and What Does It Mean in Finance?

But first, before getting down to business about different frameworks and methods, one question needs to be answered: what is a budget anyway?

From the standpoint of financial management, budget definition is simple enough: it’s a plan designed to forecast your revenue and allocate it among expenditures, saving, and objectives over a certain time period, normally monthly.

It can be thought of as a design for financial management. In the same way as how an architect plans his or her building prior to its creation, so does a budget designer his or her finances before the month commences.

Financial budgeting definition in the practical sense will consist of three main elements:

- What comes in :– your total monthly revenue

- What goes out :– your expenses both fixed and flexible

- What stays :– your savings and other investments

All three components need to be present for any budget to be truly effective.

Why Learning How to Budget Your Personal Finance Changes Everything

Here’s an example that will resonate with many of you.

Think of two colleagues, say, Aman and Priya. They get paid equally. They live in the same city, spend their salaries equally too. But after five years, Priya has saved up $14,000, has no high-interest debts and needs just two more years to save up enough for the down payment on a house. Aman has $400 in her savings account, two maxed credit cards and absolutely no plan.

The reason? Priya started managing her money in her mid-20s and continued doing so. Aman thought he would figure it out one day.

It’s not about the income but rather about your intentions.

Knowing how to manage your personal finances provides you with:

- Clarity :– you always know where your money goes

- Control :– you define your decision based on priorities rather than your on your feelings.

- Confidence :– you can make financial decisions confidently rather than nervously

- Freedom :– with a clear strategy, you won’t feel bad about splurging on things you really want

- Security :– thanks to your reserves, you don’t have to be afraid of anything

That’s why budgeting is so central to any area of personal finance – it’s not a part of the process; it’s the process itself.

How to Get Your Finances in Order Start Here

The first point in creating the personal budget plan is understanding your current situation precisely. No assumptions, no guesses. The bare facts.

And here are the steps that must be taken at the very beginning of your budget journey:

Step 1 :— Calculate Your True Monthly Income

Count every Money you have earned from any sources each month:

- Main Income (net income/take-home pay/Salary)

- Side incomes (freelancing, consulting, other business)

- Income from investments (dividends, interest)

- Rental income (from renting a flat/apartment)

It’s the budget starting point.

Step 2 :— Make a List of All Expenses

That’s what scares many people – there’s nothing to hide:

- Monthly fixed expenses: rent/mortgage, car loan payment, car insurance, etc.

- Monthly variable expenses: shopping, eating out, going for fun and pleasure

- Other irregular expenses: maintenance costs for a vehicle, healthcare payments

Gather data from your bank/credit cards statements during the last three months, sum it all, and divide by three – the result is your actual average monthly expenses.

Step 3 :— Calculate Your Net Monthly Cash Flow

Simply: Income minus Expenses = Cash Flow

If this number is positive great. Now let’s direct that surplus intelligently. If it’s negative we have a gap to close. Either income needs to rise, expenses need to fall, or ideally both.

This three-step audit is the foundation of any solid finance management system whether you’re managing personal finances, family finances, or even a small business budget.

How to Organize Your Finances The Right Framework

Now that you understand your numbers, the next part of learning how to budget personal finance involves structuring all this information. And here’s how to organize finances in an effective manner.

The best method is to break down your expenses into three sections:

1. Necessities (Non-Negotiables)

This would include anything you cannot live without rent, utility bills, food, health insurance, and minimum debt repayments. These expenses would form your non-negotiables.

2. Wants (Good Life Expenses)

Anything which adds happiness to your life but isn’t a necessity restaurant bills, subscriptions for Netflix, gym fees, traveling costs. Not bad spending habits – just more flexible ones.

3. Financial Goals (Money Management)

This covers savings, emergency fund payments, retirement plans, investing, and paying off extra debts beyond minimum payments. This is how one distinguishes between people building wealth versus merely managing their money.

Such an organizational strategy of dividing your expenses will not only help you set up a budget and finance planner, but it is a simple yet efficient system to follow throughout.

For a deeper look at the financial mistakes that derail even disciplined people, read our article 11 Financial Mistakes That Destroy Your Wealth many of these stem directly from poor budgeting habits.

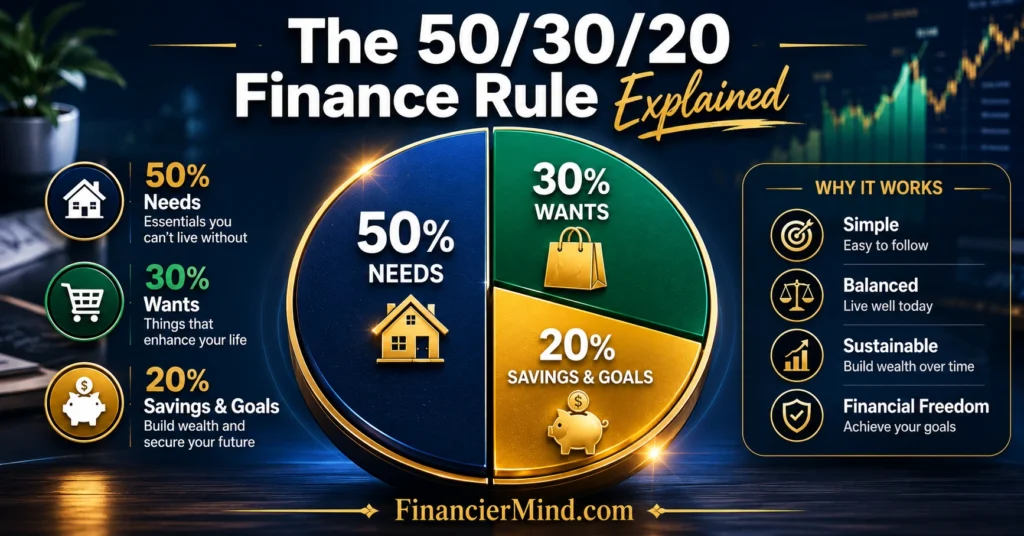

The 50-30-20 Rule The Gold Standard of Personal Budgeting

The 50-30-20 rule in finance offers a tried-and-true structure to build your budget in terms of personal finance.

Here is what that looks like:

- 50% of net income → Needs

Housing costs, food, utilities, transportations, insurance premiums, minimum debt payments

- 30% of net income → Wants

Entertainment, restaurants, vacations, leisure activities beyond basic necessities

- 20% of net income → Savings and debt repayment

Emergencies, retirement contributions, savings account contributions, additional debt repayments

A Quick Real-World Example:

If your after-tax monthly income is $4,000:

- That’s $2,000 for needs (housing, groceries, utility bills, transport costs)

- $1,200 for wants (entertainment, leisure activities, subscriptions, etc.)

- $800 for savings, investment accounts, debt repayments, and emergencies

Once again, that is not set in stone, it’s just the framework to help you start your budgeting process. If you have significant student loan debt, you may want to go for 50-20-30 approach. Or maybe you want to aggressively pay down debt, then use 50-15-35. The 50-30-20 finance rule is more about intention than execution.

The beauty of the 50-30-20 rule in personal finance is in its simple, yet efficient structure that helps you get started right away without fancy software tools and calculators. That is why educators recommend using it for years.

How to Choose the Right Budget and Finance Planner for You

Knowing the theory is one thing , but the key question here is how to apply the budgeting process to your personal finance in practice and create a system that will help you adhere to it. The following three methods can be applied depending on your personality and needs:

Option 1 :– Spreadsheet Budgeting (Perfect for Detail Oriented People)

Google Sheets/Microsoft Excel. Make a tracker with all income, fixed expenses, flexible expenses, and savings goals. Do it monthly and update weekly. Total transparency, total customization, absolutely free.

Option 2 :– Budgeting with the Help of Envelopes (Perfect for Cash Based Budgeters)

Allocate money for different categories in labeled envelopes and make sure you can’t exceed the allocated amount because when the envelope becomes empty – the money goes out. Great for people who spend too much with their credit cards.

Option 3 :– Using a Budgeting App (Perfect for Digital People)

There is a variety of apps which will do half the work for you, for example, YNAB, Mint, or Every Dollar. They connect to your accounts, categorize expenses, set the limits, and warn about exceeding them.

Option 4 :— The Zero Based Budget (Best for Maximum Control)

Every dollar of income is assigned a specific purpose until your budget reaches zero not because you spend it all, but because every dollar has a job. $0 unassigned = complete financial intentionality. This is the most powerful approach for people who want to take full control of their finances fast.

Option 5 :— The Pay-Yourself-First Method (Best for Building Wealth)

The moment income arrives, immediately transfer your savings and investment amount out of your spending account. Whatever remains is your spending budget. You never get the chance to accidentally spend what you meant to save.

The best budget and finance planner is the one you’ll actually use consistently. Start with the simplest option that fits your lifestyle consistency beats sophistication every single time.

How to Organize Personal Finances as a Family

Household budgeting is very different from individual budgeting, and this is one of the most common scenarios where financial plans fail.

This is what an effective household finance management looks like:

- Money talks must be open :– there should be no secrets here. There should be no “my money” or “your money” only one joint plan.

- A single joint budget needs to be drawn up :- at the beginning of each month. Categories must be set and limits agreed upon.

- Establish a regular financial talk :– discuss spending, make changes if needed, and see if everything goes according to plan for 20 minutes twice a month.

- Make the distinction between “household” and “personal” spending. Each person should get some personal allowance in the budget which would not require any explanation or justifications. It decreases arguments significantly.

- Think of possible irregular expenditures and save for them accordingly :– taxes, fees, holiday presents, insurance premium payments. Make sure there’s enough money for all those items every year.

The key is to feel equal in terms of finance management.

If you’re also working on improving your household credit health alongside budgeting, our full guide on How to Increase Credit Score by 100 Points walks through everything you need to know.

Advanced Strategic Finance Budget Planning for Startups and Entrepreneurs

This is the same with entrepreneurs and startup owners except the challenges faced may have varying degrees of intensity, and there are many variables involved. Planning for budget in strategic finance requires forecasting and proper allocation of cash resources.

The following are the differences between how finance managers and startup owners undertake budgeting compared to personal budgeting:

- Forecasting cash flows by finance managers in budgeting: Historical information, seasonality factors, conservative cash flow projections, and best and worst case scenarios are considered when developing a three scenario cash flow model.

- Zero based budgeting for organizations: All expenses require justifications at every cycle instead of having automatic carryovers, thus avoiding excess spending.

- Budgeting responsibility of departmental heads: It means that every team is responsible for their own budget allocations.

- Rolling forecasts vs annual budget forecasts: The smart thing to do as far as business is concerned is to have a rolling forecast of 12 months, revised monthly, instead of sticking to an annual budget which becomes outdated in March.

Whether it’s budgeting and finance for public organizations or startups, the procedure is the same.

Your Personal Finance Budget Checklist Start Today

Here is your full action checklist on getting started with how to budget your personal finance:

- Work out your precise after-tax income per month

- Gather 3 months’ worth of bank and credit card statements

- Categorize expenses into needs, wants and goals

- Implement the 50-30-20 formula as the basis of your budget

- Pick your budgeting approach and stick to it. (spreadsheet, app, etc.)

- Make automatic deposits to your savings account once you receive your pay

- Create a budgeting schedule every month beginning on the first day

- Have a bi-weekly check-in with yourself (or with your partner)

- Start a sinking fund to cover yearly expenses

- Reassess and revise your budget on a quarterly basis as necessary

Implementing these steps faithfully is truly what it takes to learn how to budget your personal finance. It isn’t a one-off exercise it involves deliberate action on your part every month.

Want to go deeper with official government-backed budgeting worksheets and financial planning tools? The U.S. Federal Government’s dedicated financial literacy portal has everything you need from monthly budget calculators to step-by-step spending planners all completely free. Visit: MyMoney.gov Official U.S. Government Budgeting & Financial Planning Tools

Understanding how to read financial ratios will help you level up beyond budgeting. See our in-depth guide: The Ultimate Guide to Finance Ratios for Better Understanding

The Expenses Personal Finance Definition Why It Matters

What might confuse beginners when learning about the personal finance definition is the concept of expenses more precisely, differentiating between an “expense” and payment for the achievement of a financial goal.

This is the difference:

- An expense is money used on consumption spending on food, rent, entertainment, subscriptions. Money spent, without any value to come back in the future.

- The money transferred into savings or investments is money used to create future value money deposited to an emergency fund, retirement savings account, or other types of investments. It’s not an expense. It’s investing in your own wealth.

- Understanding the difference between those two terms will change how you perceive and deal with both concepts. Once you stop thinking of the money transferred to savings as “the money that I lost” and start looking at it as “the money I’m paying myself in the future,” you will fundamentally alter your attitude toward personal budgeting.

Which makes complete sense once you understand the whole finance management system of personal budgeting.

Brief Summary

Step 1 :— Calculate Your True Monthly Income

Step 2 :— Track and List Every Expense Honestly

Step 3 :— Calculate Your Net Monthly Cash Flow

Step 4 :— Categorize Everything into Needs, Wants & Goals

Step 5 :— Apply the 50-30-20 Rule as Your Framework

Step 6 :— Choose Your Budget and Finance Planner System

Step 7 :— Schedule Monthly Reviews and Quarterly Audits

Frequently Asked Questions

1. What is the best way to start budgeting my personal finances as a complete beginner?

Begin by finding out how much money you take home every month.

Get 3 months of bank statements and find how much on average you spend in each category per month.

Budget your finances using the 50-30-20 rule that means putting 50% towards needs, 30% towards wants, and 20% towards savings and goals.

Choose one basic tool for tracking your money and do it once every week.

Most importantly, just begin, however imperfectly, and improve your approach gradually.

2. How do I get my finances in order if I’m already in debt?

Consider the full picture first by writing down all your debts, how much you owe for each one, the interest rate, and the minimum payment due on each.

Then include all your minimum payments under “Needs” because that way you won’t miss paying them.

After you have paid everything in your “Needs” budget, apply any additional money you might have towards paying off the highest interest debt first or the smallest balance for psychological victories (avalanche or snowball methods).

Save an adequate sum every month for paying off debts, maybe $50 or more.

3. How does the 50-30-20 rule work in real life with a tight income?

The 50-30-20 plan is just that; feel free to mold it to fit you.

If your needs take up 65% of your money, begin by using a 65-15-20 framework and working to lower needs.

What’s non-negotiable about this plan is the 20% savings/goals amount; even if you have only 5% or 10%, the process is more important than the exact figure.

Increase the savings/investments amounts as you earn more or repay debts to slowly shift towards the ideal 50-30-20 distribution.

4. What is the difference between a budget and a finance management system?

The budget is the monthly plan; this is where your income is allocated into various buckets, and spending is compared against goals.

The finance management system is the whole structure that surrounds the budget. This system includes everything from your budget to savings plan, investments, debt repayment schedule, insurance coverage, and periodic financial evaluation.

See your budget as only part of the overall financial management system. Budgeting is an activity, while the financial management system is an architectural concept.

Eventually, the finance management system will become more complex and will involve tax planning, investment reallocation, estate management, and other sophisticated operations – but always start with the simple budgeting process.

5. How often should I review and update my personal finance budget?

Monthly: Start fresh, creating a new budget every month because budgets are not static, and incomes and expenditures change.

Bi-weekly: Take a look at whether you are meeting budgeting targets in your spending and adjust if you’re over budget in some areas.

Quarterly: Take time for an in-depth analysis and see if the goals are appropriate, if your income has changed, and if your savings goals have changed.

Annual: Take the time to assess how well you did over the entire year; conduct an annual net worth assessment, evaluate your savings rate, your insurance needs, and investments.

Budgeting is not about writing things down once, but rather reviewing your budget often.

Disclaimer: The information in this article is for educational purposes only and is not intended as personal financial advice. For guidance specific to your financial situation, please consult a certified financial planner or advisor.

About Financier Mind: We’re here to make financial education genuinely useful — from your first budget to your first investment. If this guide helped you, share it with someone who’s still figuring out where their money goes every month. 💸