This article is written specifically for the USA audience and is based entirely on the American credit scoring system, primarily the FICO Score model, which is the standard used by most lenders across the United States.

If you’re reading this from India, the UK, Canada, Australia, or any other country your country likely has its own credit bureau system. For example, India uses credit scores from bureaus like CIBIL, Experian India, Equifax India, and CRIF High Mark, and the scoring range and factors may differ from what’s described here.

However :— here’s the good news: The core financial strategies shared in this article such as paying on time, keeping your utilization low, managing collections, and understanding how credit limits affect your score are universally applicable principles. No matter which country you’re in, these fundamentals of responsible credit behavior hold true.

So if you’re outside the US, simply apply these strategies in the context of your own country’s credit system, and you’ll still find tremendous value in this guide.

Now, let’s get into it. 👇

Let me ask you one thing the last time you checked your credit score what was the result? Did you find it satisfactory and reassuring or made you nervous?

I am pretty sure that you clicked the link above because you are looking for some advice on how to increase credit score effectively and permanently. It should not be just a temporary change for one transaction, but rather a long-term solution to improve your financial future, as your credit score determines such things as mortgage, loans, renting possibilities, even credit cards.

The fact I will not tell you in many financial articles is that it is possible to improve your credit score, and you will know how to do it; however, it needs consistency in following the steps. No secrets are needed – all you need is to learn how it all works.

This post aims to explain everything about how to increase credit score significantly, sometimes by up to 100 points in a relatively short period of time, to give examples, answers to possible questions you have, and provide a detailed plan for increasing credit score.

Let us get started.

What Does It Mean to Increase Credit Score And Why Does It Control Your Life?

Your credit score is a three-digit number, which is usually generated using either FICO or Vantage Score, and which falls somewhere within the range of 300 to 850. The larger your number, the bigger the chances are more that lenders will consider you financially responsible.

This is a brief overview of the ranges:

- 800-850 = Excellent; the best possible interest rates for anything you buy

- 740-799 = Very good; high chance of approval

- 670-739 = Good; acceptable approval rate; average interest rates

- 580-669 = Fair; difficult but not impossible to get credit

- 300-579 = Poor; few chances of obtaining any credit

If just by increasing your credit score by a mere 40 or 50 points, you will shift into another category, this will mean a lot of money saved since such a change may save you thousands of dollars in interest charges.

Take the case of two individuals taking out mortgages for the same amount of money. For example, both have taken out a mortgage of $300,000, for 30 years. If the first individual has a Fair score of 620, he might be quoted an interest rate of 8.2%, but the second individual, who has a Very Good score of 760, may get an interest rate of 6.5%. Over a period of 30 years, the first individual ends up paying over $120,000 in excess charges. This is why it is important to learn about how to improve credit score.

How Quickly Can Your Credit Score Increase?

This is another very frequently asked question that hinges entirely on what the reason is for your poor scores in the first place.

Here’s an approximate timeline of when you can likely experience a change in your credit score:

- Repaying the high credit card balance (credit utilization amount): In this case, expect improvements in just 30-45 days, which is about one billing cycle since your new balance is reported.

- Dispute successfully resolving a reporting error on your report: Improvements should be made within 30-60 days after the resolution.

- Closing a collection account: Changes in scores because of closing such accounts should come into effect within 1-3 months.

- Becoming an authorized user on a positive account: In this case, results might become noticeable in 30-60 days, although in some cases, quicker results may be seen.

- Building credit from scratch through secured cards: Results will take 6-12 months of demonstrating good habits.

As you may notice, some actions lead to quicker results than others. The fastest way to improve credit score is by fixing issues related to credit utilization and disputing negative reports on your record.

“Don’t cut up your credit cards, the problem is not the cards, it’s the lack of financial literacy of the person holding the cards”.

Robert Kiyosaki – (Author of Rich Dad and Poor Dad)

When to Pay Your Credit Card Bill to Increase Credit Score

This is one that tends to shock many individuals timing really does matter when it comes to paying off your credit cards.

The thing is, when it comes to your credit score, credit card companies will generally report your account balance to the credit reporting agencies on the statement closing date, not your payment due date. This means if your statement closing date falls on the 15th and your payment due date on the 10th of next month, your account balance reported will be whatever you had remaining from the 15th.

The strategy to increase credit score through timing:

- Pay your balance before your statement closing date, not just before your due date. This way, the bureaus see a low or zero balance, which improves your credit utilization ratio instantly.

- Aim to keep your reported utilization under 10% per card for maximum scoring impact. Under 30% is the common advice, but under 10% is where the real score jump happens.

- If you carry any balance at all, try to make two payments per month — once mid-cycle to knock down the balance before it reports, and once on the due date to avoid interest.

Real-world example: Sarah had a credit card with a $5,000 limit and consistently carried an $1,800 balance. Her utilization was 36% dragging her score down. When she started paying mid-cycle to bring the reported balance to $300 (6% utilization), her score jumped 27 points within a single billing cycle without paying off any additional debt. Same money, different timing.

How to Increase Credit Score by 100 Points The Step-by-Step Blueprint

This is the section you’ve been waiting for. Here’s a systematic, prioritized approach to increase credit score by 100 points or more over time.

- Step 1 :— Pull All Three Credit Reports and Audit Them

Get your free reports from AnnualCreditReport.com (the only federally authorized free source). Look for errors wrong balances, accounts you don’t recognize, late payments that were actually on time. Dispute every error you find directly with Equifax, Experian, and TransUnion. Incorrect information on reports is more common than people think, and removing it can increase credit score significantly with zero additional effort.

- Step 2 :— Slash Your Credit Utilization Rate

This single factor is responsible for 30% of your FICO score. If you’re using more than 30% of your available credit across all cards, this is your fastest lever. Pay down balances, ask for a credit limit increase (more on this soon), or spread existing balances to underutilized cards.

- Step 3 :— Never Pay Late again – Set Up Auto Pay – Your payment history makes up the largest chunk of your credit score, accounting for 35% of the FICO score calculation process. Just one 30 days late payment can lower your credit score instantly by anywhere between 60 and 110 points. Make sure you set autopayment for all payments in order to avoid missing them.

- Step 4 :— Keep All Your Old Accounts – Your credit age is what determines 15% of your credit score. Closing an older account will have a negative effect both on your average credit age and utilization ratio. Only if the account charges a high annual fee should you consider closing it otherwise just make sure to use it once in a while.

- Step 5 :— Apply For New Credit Carefully – Applying for new credit results in what’s called a hard inquiry. Each hard inquiry is worth around 5 to 10 points and lingers on your report for up to two years. In case you’re trying to boost your score, avoid applying for any form of credit until you no longer need it.

- Step 6 :— Diversify Your Credit Portfolio – A credit profile with a good blend of revolving and installment credit accounts demonstrates to the lender that you know how to handle different kinds of credit. It constitutes 10 percent of your credit score, and even if you do not feel compelled to take up debt for the purpose of diversification, you should be mindful of it.

- Step 7 :— Consider Getting a Secured Credit Card or Credit-Builder Loan – For people whose credit scores are less than 600, such options are especially beneficial, and they are created with thin-file or damaged-credit consumers in mind.

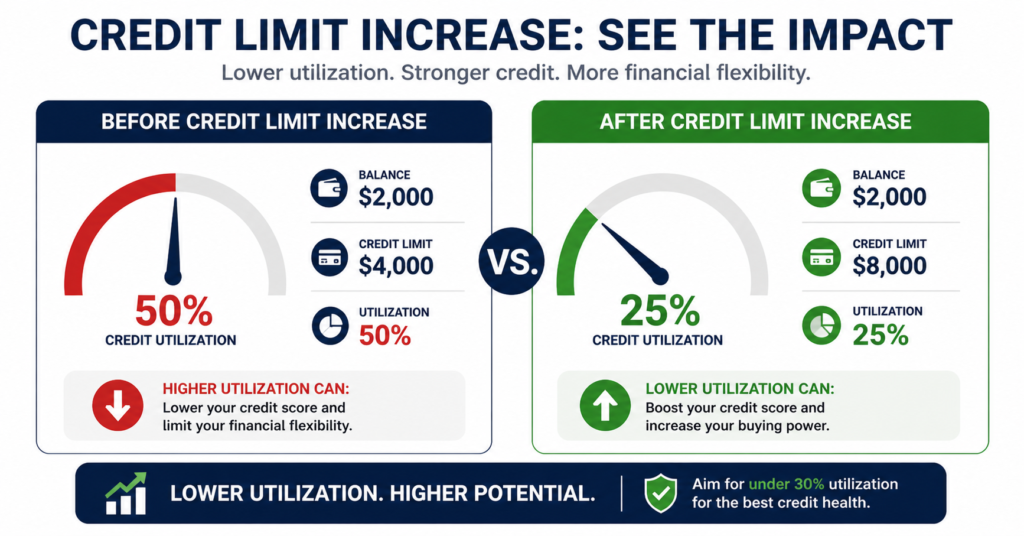

Does a Credit Limit Increase Affect Credit Score?

Well, it’s time to clarify this matter as it arises all too often. Is it possible for credit limit increase to influence the score negatively? Well, yes it might – but only in one case!

Namely, when your credit limit goes up while the balance remains the same, your credit utilization ratio automatically goes down. Utilization makes up 30% of your FICO score, thus the lower ratio equals higher score.

For example, if you have a $2,000 balance on the card with a $4,000 credit limit (that’s 50%), your limit increases to $8,000 but balance remains the same, utilization will decrease to 25%. And that’s a good reason to expect at least 20–40 increase in your credit score.

However, is credit limit increase hurting credit score before bringing it benefits?

The matter of fact is that credit limit increase request will most likely cause the lender’s hard inquiry to take place, which will reduce your score slightly. On the other hand, nowadays a lot of banks perform soft inquiries, which have zero effect on the FICO score (though not all of them). So, make sure to ask the bank about the nature of their limit check procedure.

Will Requesting a Credit Line Increase Affect My Credit Score?

As stated above yes potentially, although not necessarily. Let’s take it one step further and go into specifics so that you can understand what you are getting into.

When it’s a soft pull (no impact on credit score): Some issuers such as Capital One, Discover, and American Express have a policy where they automatically increase limit as part of account review or offer the ability to increase limit via app without hard inquiry on your credit report.

When it’s a hard pull (temporary drop): Sometimes, the lenders use a hard inquiry when processing a limit increase, especially when dealing with a bigger request. This leads to a small 5-10 point drop in the credit score lasting around 12 months and then disappearing completely after 2 years. Most often than not, the benefit from low utilization is going to be much greater than this brief decline.

Tip: Before making the request, make sure to call your card issuer’s customer support and specifically ask: “Is this going to result in a hard inquiry being done on my credit report?” They will be obligated to tell you whether this is the case.

Want to understand the full picture of what’s hurting your financial health? Read our article on 11 Financial Mistakes that destroys your Wealth many of these directly tie into your credit habits.

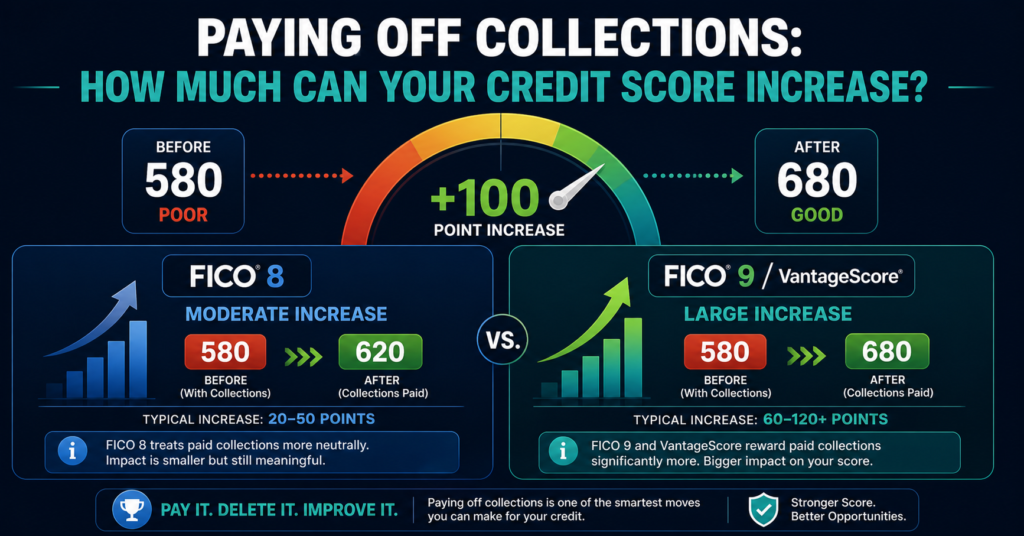

How Much Will Credit Score Increase After Paying Off Collections?

However, it all hinges largely on which credit scoring formula is applied by your lender which is an absolutely crucial difference.

In case of FICO 8 (by far the most popular formula):

Your paid collection will remain on your report and still have a negative effect on your score, even though it is not as big as that of an unpaid collection. Being paid, the collection becomes less damaging and more acceptable. With FICO 8, paying off your debt may only raise your score 5-20 points.

As for FICO 9 and VantageScore 3.0/4.0:

These formulas completely disregard the paid collections, meaning that once you clear a collection account, its effects disappear entirely and your score rises sharply as a consequence. In some cases, paying off a collection under these formulas may raise your credit score 30-80 points!

Knowing about this, you should take into consideration the following facts before deciding to clear your debt:

- Your lender’s chosen scoring model

- The possibility of negotiating a “pay-for-deletion” with the collection agency

- Whether the collection is out of statute in your state

A paid or deleted collection is one of the quickest legal methods of significantly boosting your credit score.

For official FICO scoring factor breakdowns, refer directly to: What’s in my FICO Scores?

Student Loans And Credit Score What You Should Know

The thing about student loans is that these credits can be beneficial and harmful for you at the same time.

The actual impact of student loans on your credit score is as follows:

- Payments are positive factors installment loans will improve your payment history and credit mix.

- Paying back all the loans may negatively affect credit score – this is something most people cannot believe. Once you fully repay the loan, you no longer have any open installment account in your credit mix, which means that there might be a slight reduction of your score.

- Recent changes in Income-Driven Repayment plans affected credit scores for some borrowers recent changes in loan repayment plans have caused fluctuations in balance utilization rates and other important credit metrics.

- Refinancing a student loan might be negative once you refinance your loan, the initial credit account is closed, while the new loan has just opened. It also causes hard inquiry and affects your average account age.

So, it might be stated that, in general, student loans have a positive effect on credit scores.

To understand your overall credit profile more deeply, don’t miss our beginner-friendly deep dive: Credit Score explained how to improve it safely.

Real-Life Illustrations That Demonstrate the Success of These Strategies

- Case Study 1 – Marcus, 28, Credit Score: 591 → 714 in 9 Months

Marcus had two late payments from 2021, a 68% utilization ratio for his three credit cards, and one minor collection account. He settled the collection account with a pay-for-deletion strategy for $340, brought down his credit card balances such that the overall utilization became less than 15%, and enabled autopay on all his accounts. Within nine months, his credit score increased by 123 points, which was good enough for him to get prime auto loan rates.

- Case Study 2 – Priya, 35, Credit Score: 643 → 724 in 4 Months

In Priya’s case, her credit score was solely driven by utilization since she was making timely payments. She used 72% of her credit card limit and had an otherwise flawless record. She got her two credit card companies to agree to limit increase requests via soft pulls, both of which were granted. In addition, she made a lump-sum payment to lower her utilization to 11%. After four months, her credit score crossed the mark of 720, enabling her to refinance her home loan and save $214 per month.

FAQ’s

1. How much time will it take for me to improve my credit score by 100 points?

The sooner that all these problems are sorted out by the user, the faster their credit score improves.

If you begin with their score in the range of 580-620, then it will only take about 6-18 months to get an improvement of 100 points in the credit score.

Quick solutions such as reducing the utilization ratio and handling disputes will enable one to achieve a score in 30-60 days.

Structural changes, including removing collections and building payment history, will take 6-12 months.

2. Does credit limit increase instantly improve credit score?

Within 60-90 days, there should always be a positive net effect.

Indeed it does, although it depends. In case of reporting an increased credit limit to credit bureaus and not changing one’s balances, the utilization ratio will decrease, thus improving credit score within one billing cycle (30 days).

In case the application for a credit limit increase led to a hard inquiry, then one’s score will go down by 5-10 points first and then start to grow after that.

3. Will requesting a credit line increase affect my credit score?

Always call and ask your issuer which type they’ll use before submitting the request.

It depends on whether your lender uses a hard or soft inquiry.

Soft inquiry = no score impact at all.

Hard inquiry = small temporary dip of 5–10 points, typically recovering within 12 months.

4. By how many points would my credit score increase after paying off collections?

The best way to proceed: First try negotiating for pay for deletion.

With the FICO 8 scoring model (which most lenders use): Paying off the debt could lead to a small boost of about 5 to 20 points, since the debt will be reported even when paid off.

With the FICO 9 and Vantage Score 3.0/4.0 scoring models: The paid collections aren’t considered at all, and you’d see an improvement of up to 30 to 80 points.

5. When is the best time to pay a credit card bill to increase credit score?

If your issuer reports on your closing date, even paying 2–3 days early makes a measurable difference.

The best time is before your statement closing date — not just before your payment due date.

Paying before the closing date means a lower (or zero) balance gets reported to the credit bureaus.

This directly reduces your reported utilization, which can boost your score within the very next billing cycle.

Note: This article contains general information intended for educational use only and should not be considered financial or credit counseling advice. Credit score results will differ from person to person. It is recommended that you seek professional financial or credit counseling help.

About Financier Mind: We’re on a mission to make financial knowledge accessible to everyone — from beginner to advanced. If this article helped you, share it with someone whose credit score could use a lift. 💳

1 thought on “Increase Credit Score by 100 Points Proven Blueprint Everyone Needs Right Now!”